Table of Content

The person with the HELOC can borrow up to a certain maximum amount at whatever time they choose. If you’re in need of a large sum of cash on a revolving basis to keep up with your home improvement needs, a HELOC could be a good choice for you. If you know the exact amount of money you need for a project and prefer a fixed monthly payment plan, then a home equity loan may be the better option. If you aren’t interested in opening a home equity line of credit, you still have options for tapping into your home’s equity. A cash-out refinance is one of the easiest ways to access the cash in your home without taking on an entirely new loan. Medical bills can easily run thousands of dollars for even the most basic procedures and care.

In addition, financial advisors/Client Managers may continue to use information collected online to provide product and service information in accordance with account agreements. Learn about how a home equity line of credit works and how it may help you realize your goals – from covering unexpected expenses to paying for educational costs and funding home renovations. The RBC Mortgage Add-On option lets you access additional funds by adding them onto your existing RBC Royal Bank mortgage, based on the current appraised value of your home.

How to Calculate Your Home Equity

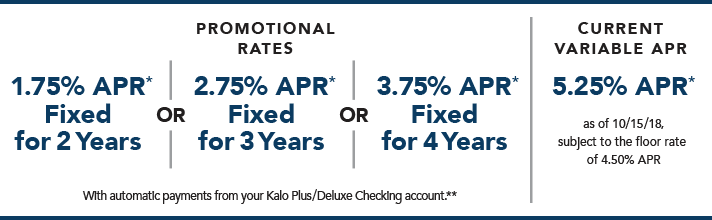

Once the draw period ends, the person cannot access money from the line of credit. 5The advertised rate will vary if the client chooses for the bank to pay their closing costs, which is an option in some states if the requested loan amount is less than or equal to $500,000. Other fees may be charged at origination, closing or subsequent to closing, ranging from $0 to $10,000, and may vary by state. If you pay off your Truist Home Equity Line of Credit within 36 months from the date of loan origination, you may be required to remit any closing costs Truist paid on your behalf. There is a $50 annual fee in AL, AR, CA, FL, GA, IN, KY, NJ, and OH.

One way to tap into that value is with a home equity line of credit . Here’s a closer look at what a home equity line of credit is, how it works and what it can be used for. The best rate discounts are reserved for Preferred Rewards members and those who make large draws from their HELOCs. The realtor.com® editorial team highlights a curated selection of product recommendations for your consideration; clicking a link to the retailer that sells the product may earn us a commission.

Home Equity Loan vs. HELOC: What’s the Difference?

Loan-to-value ratio is the percentage of your home's appraised value that is borrowed - including all outstanding mortgages and home equity loans and lines secured by your home. For example, a lender's 80% LTV limit for a home appraised at $400,000 would mean a HELOC applicant could have no more than $320,000 in total outstanding home loan balances. Remember, the $320,000 limit would include all existing loans secured by your home plus your new HELOC.

A home equity loan provides you with a one-time lump sum payment that allows you to borrow a large amount of cash and pay a low, fixed interest rate with fixed monthly payments. Paying off a mortgage with a home equity line of credit is technically possible. It is essentially a way of refinancing your loan, but actual refinancing is a much simpler option for reducing an interest rate on a mortgage to pay it off more quickly.

Jobs and Making Money

So in the example above, you'd be able to establish a line of credit of up to $80,000-$90,000 with a home equity line of credit. You need a credit score of at least 660 to qualify for most Home Equity Loans, while a score of 720 and above puts you in an excellent place to access the loans. An equity line of credit calculator shows you how much you can borrow based on your current home equity. It also clarifies how that amount will vary with a change in the value of your home.

So, as with every type of home loan out there, it’s best to be cautious and do your homework. Is that a HELOC borrows against the existing equity in your home, while the latter does not. Because of this, home improvement loans have a lower limit that you can borrow. These loans can also carry higher interest rates than HELOCs.

Flagstar Bank: Best home equity line of credit for good credit

To calculate the equity on your home, subtract the amount owed in mortgage loans for the home from the current appraisal value of the home. You can then express this as a percentage of the appraisal value of the home to compare with the 20%. You can calculate home equity by subtracting the amount owed due to the mortgage from the current estimated value of the house. You may also make use of our Home Equity Line of Credit Calculator to determine further how much you can borrow based on your current home equity. Simple – Your loan's rate, term and amount of the loan are all fixed, so you can rest easy knowing your payments will stay the same and your rate won’t go up. Stable – Your loan’s rate, term and amount are all fixed, so you can rest easy knowing your payments will stay the same and your rate won’t go up.

We are not seeing any trends in the HELOC market that are going the ways of Wells Fargo and Chase. In fact, the HELOC market is getting a lot more aggressive in their offering and loosening some guidelines. We do anticipate that banks will get a little more conservative on max loan-to-value leverage ratios when they see home values start to plateau.

Conversely, HELOCs allow a borrower to tap into their equity as needed up to a certain preset credit limit. HELOCs have a variable interest rate, and the payments are not usually fixed. Because both home equity loans and HELOCs use your home as collateral, they usually have much better interest terms than personal loans, credit cards, and other unsecured debt.

Please consult your tax advisor regarding interest deductibility as tax rules may have changed. If you have a good credit score, you’ll have a better chance of qualifying for the lowest rates available, which will reduce your overall loan cost. It enables them to withdraw within a specified period from when they open their accounts. This timeframe is known as the draw period, which is between years. During the draw period, borrowers can borrow but need to make timely payments.

A HELOC can be a worthwhile investment when you use it to improve the value of your home. However, when you use it to pay for things that are otherwise not affordable with your current income and savings, it can become another type of bad debt. One possible exception to this “rule” is in the event of a true financial emergency (as long as you are confident that you’ll be able to make the payments). In addition to the standard mortgage calculator, this page lets you access more than 100 other financial calculators covering a broad variety of situations. Choose from calculators covering various aspects of mortgages, auto loans, investments, student loans, taxes, retirement planning and more. To take out a home equity loan, you should first check to see that you're eligible for the loan based on your home equity and credit score.

No comments:

Post a Comment